Overview

Project cost management (PCM) is a method that uses technology to measure cost and productivity through the full life cycle of enterprise-level projects

PCM encompasses several specific functions of project management including estimating, job controls, field data collection, scheduling, accounting and design.

Beginning with estimating, a vital tool in PCM, actual historical data is used to accurately plan all aspects of the project. As the project continues, job control uses data from the estimate with the information reported from the field, to measure the cost and production in the project. From project initiation to completion, project cost management has an objective to simplify and cheapen the project experience.

This technological approach has been a big challenger to the mainstream estimating software and project management industries.

Project Cost Management is one of the ten Knowledge Areas outlined in the A Guide to the Project Management Body of Knowledge (PMBOK Guide). It is used during the Planning and Monitoring & Controlling Process Groups.

Estimating the Costs

The first step in cost management is to estimate the costs of each activity in the project. Costs include both human resource and physical resource costs. Because this step often occurs in the planning phase, it is important to understand that the estimated costs are your “best guesses” at the actual costs of each activity.

To undertake an informed guess at the costs you can use one of the following techniques:

- Analogous Estimating: estimates are based on past projects. It uses actual costs from a similar completed project to estimate the costs of the new project. The accuracy of these estimates will depend on the similarities between the new project and the old project.

- Parametric Modeling: estimates are based on mathematical formulas, typically following a Regression Analysis or Learning Curve model. The accuracy of these estimates depends on the assumptions made.

- Bottom-up Estimating: estimates are based on the individual work item cost and duration estimates. This involves estimating the smallest activities and then adding them up to create an estimate for the whole project.

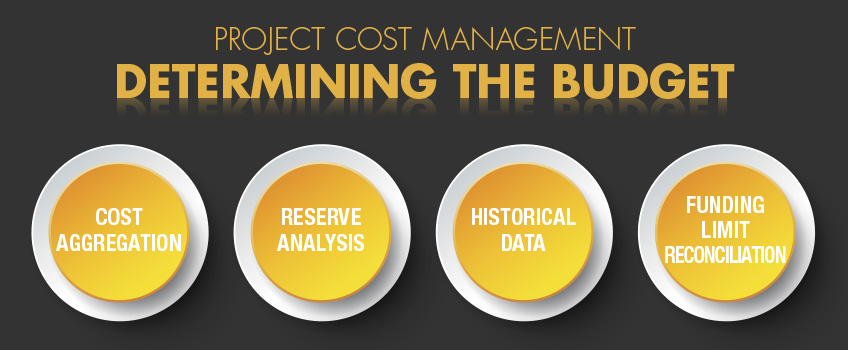

Determining the Budget

Using your best-guess estimates, the next step is to create a realistic project budget. In this step, you will determine the cost baseline and the funding requirements for the project. A good project budget will help you make key decisions with respect to the project schedule and resource allocation constraints.

To determine the project budget, the PMBOK suggests using several techniques:

- Cost Aggregation: requires you to aggregate or combine costs from an activity level to a work package level. The final sum of the cost estimates is applied to the cost baseline.

- Reserve Analysis: requires you to create a buffer or reserve to protect against cost overruns. The degree of protection should be equivalent to the risk foreseen in the project. The buffer is part of the project budget, but not included in the project baseline.

- Historical Data: requires you to think about estimates from closed projects to determine the budget of the new project. This is very similar to the analogous estimation described earlier.

- Funding Limit Reconciliation: requires you to adhere to the constraints imposed by the funding limit. The funding limit is based on the limited amount of cash dedicated to your project. To avoid large variations in the expenditure of project funds, you may need to revise the project schedule or use project resources.

Controlling the Costs

Good project managers will carefully monitor the cost of their projects. This includes watching to see where the actual cost has varied from the estimated cost. Cost control also involves informing the stakeholders of cost discrepancies that vary too much from the budgeted cost.

To effectively control project costs, you will need to regularly monitor and measure the performance of the budget and revise forecasts as required. The PMBOK suggests several tools and techniques help control costs:

- Earned Value Management: uses a set of formulas to help measure the progress of a project against the plan.

- Forecasting: uses the current financial situation to project future costs. The forecast is based on budgeted cost, total estimated cost, cost commitments, the cost to date, and any over or under-budgeted costs.

- To-Complete Performance Index (TCPI): represents the level of project performance that future work needs to be implemented to meet the budget.

- Variance Analysis: This involves analysing the difference or variance between the budgeted costs and the actual costs to indicate whether the project is on budget.

- Performance Reviews: used to check the health of a project. Includes an analysis of project costs, schedule, scope, quality, and team morale.

References

- A Guide to the Project Management Body of Knowledge (PMBOK Guide) – Fifth Edition

- Jessie Warner, 30 November 2010, Understanding Project Cost Management

- Wikipedia

How CBIS can help you

Please contact us if you need more details on how our expert team can assist you. We are simply experts in the cost management of Lean Six Sigma projects.

01 Jul 2021

LEARN WITH CBIS What We Offer

Attending our Public classroom physically or joining the team virtually from anywhere, according to the training calendar.

A flexible self-paced training for busy people along with our support by a dedicated coach, to solve the disadvantage of one-way online training

Delivering flexible and tailored training for your team and at your premises as a cost-effective solution for your team.

Send us a Message Make an Enquiry

Your Cart